For any bank or fintech weighing eKYC Vietnam options against legacy paperwork, the timing matters. Since Vietnam's Decree 94/2025/ND-CP took effect on July 1, 2025, the country's fintech sandbox has been officially operational - and banks and fintech companies are now optimizing their onboarding flows in this new regulatory environment. The central question for every product team is the same: eKYC or stick with manual onboarding?

The urgency is not coincidental. The Personal Data Protection Law (PDPL), effective January 1, 2026, tightens requirements on how identity data is collected and processed. Vietnam's AI Law (effective March 1, 2026) sets new standards for automated verification systems. Amid this regulatory wave, the cost and risk of manual onboarding grows every month.

This article, from the DataCore blog, directly analyzes the three dimensions that CFOs, Product Managers, and Risk Officers in Vietnam's financial sector care most about: speed, cost, and regulatory compliance.

What Is eKYC Vietnam and Why It Matters

eKYC (Electronic Know Your Customer) is a fully digital customer identity verification process - no in-person meeting required. An eKYC system combines three technology layers:

- OCR (Optical Character Recognition): extracts information from ID card/passport images

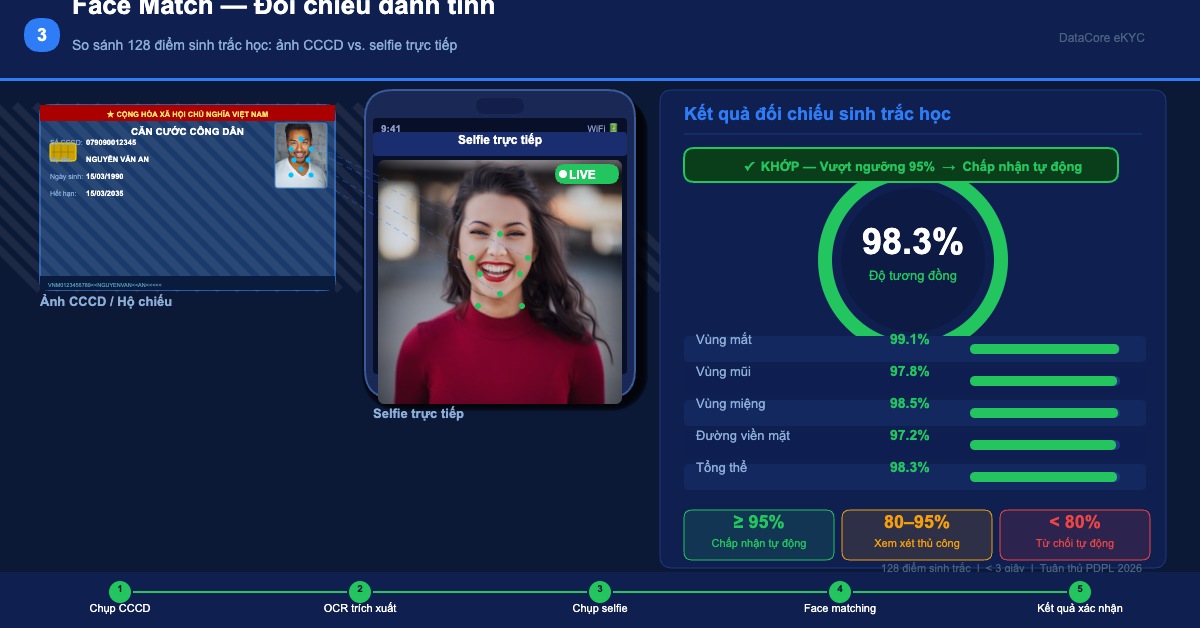

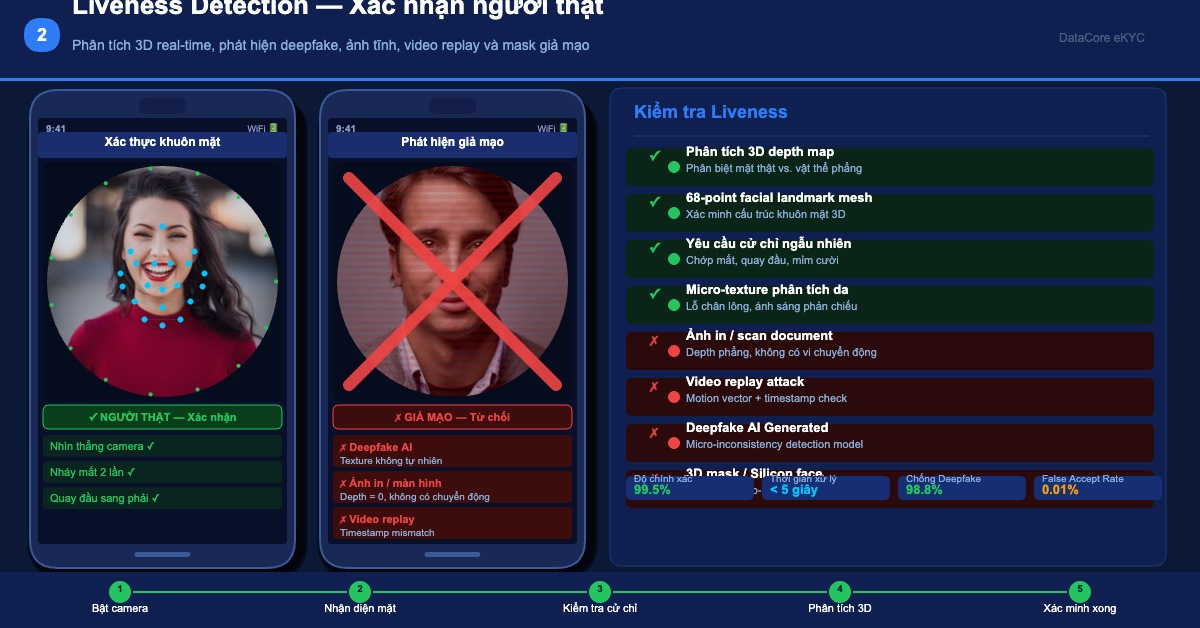

- Face matching & liveness detection: cross-references the face with the document, detects deepfake or static image fraud

- Database verification: cross-checks against the national citizen database (VNeID), AML lists, and tax/company data

In Vietnam, eKYC has been licensed by the State Bank under Circular 16/2020/TT-NHNN. By 2026, this is no longer an "optional upgrade" - it is the required infrastructure for genuine digital financial operations.

Head-to-Head: eKYC vs. Manual Onboarding

| Criterion | Manual Onboarding | eKYC (API) | Winner |

|---|---|---|---|

| Onboarding speed | 2-5 business days | 30-90 seconds | ✅ eKYC - 200x faster |

| Cost per customer | VND 150K-400K | VND 8K-25K | ✅ eKYC - 80-95% savings |

| Accuracy | 85-90% (human-dependent) | 97-99.5% (AI-driven) | ✅ eKYC - fewer errors |

| PDPL 2026 compliance | High risk - physical document storage | Compliance-by-design - encrypted, audit log | ✅ eKYC |

| Scalability | Linear with headcount | Auto-scales with volume | ✅ eKYC - unlimited scale |

| Customer experience | Branch visit or file upload required | 100% mobile, 24/7 | ✅ eKYC - superior UX |

| Initial integration cost | Low (existing process) | Medium (API integration 2-4 weeks) | ⚖️ Manual - lower upfront |

| Fraud risk | High - hard to detect sophisticated fraud | Low - liveness detection, deepfake filter | ✅ eKYC |

Speed: From 5 Days to 60 Seconds

A typical Vietnamese retail bank's manual onboarding involves: customer visits branch (or uploads files), staff checks documents, enters data into the system, compliance review, then account activation. Average 2-5 business days - in the best case, no errors.

With eKYC, the entire process happens in 30-90 seconds on a smartphone: photograph front/back of national ID → OCR extracts data <2 seconds → selfie + liveness check <5 seconds → face matching <3 seconds → database check (VNeID + AML) <10 seconds → instant account activation.

When time-to-active drops from 2 days to 60 seconds, onboarding funnel drop-off decreases by an average of 60-70%. Southeast Asian fintech platforms that have deployed eKYC report conversion rates rising from 35-45% to 70-85%.

Cost: A Real TCO Analysis

| Cost Item | Manual Onboarding | eKYC API |

|---|---|---|

| KYC analyst headcount | VND 150K-250K/file | 0 (automated) |

| Physical document storage | VND 15K-30K/file/year | 0 (cloud, encrypted) |

| Error & reprocessing costs | VND 50K-100K/error (10-15% of cases) | Near 0 (AI accuracy 97-99.5%) |

| PDPL violation risk | High potential (fines up to 5% of revenue) | Low - encrypted, full audit trail |

| API call cost | - | VND 8K-25K/verification |

| Average total per file | VND 215K-380K | VND 8K-25K |

At 10,000 new customers per month - not unusual for growing digital banks - this difference equals VND 1.9-3.5 billion in monthly savings. The initial eKYC API integration cost (VND 40-80 million) is typically recovered within 1-2 months.

Regulatory Compliance: PDPL 2026 and the AI Law

The Personal Data Protection Law (PDPL) - effective January 1, 2026 mandates: biometric data (facial images, ID cards) is "sensitive data" requiring encryption and time-limited retention; a right-to-erasure mechanism; and full audit logs of every data access. Penalties reach 5% of revenue or VND 3 billion.

Vietnam AI Law - effective March 1, 2026 requires: AI systems used in identity verification must classify risk levels, provide explainability for decisions, avoid discrimination, and maintain audit logs for inspection.

Manual onboarding with physical documents or scanned files stored on internal servers typically violates at least 2-3 PDPL provisions: lack of encryption, missing audit logs, and indefinite retention without clear time limits.

Three Real-World Scenarios in Vietnam

Scenario 1 - Retail bank going digital: 80-person KYC team processing 15,000 files/month at ~VND 225M/month cost. After eKYC: cost drops to ~VND 150M/month; team shifts to higher-value tasks.

Scenario 2 - Fast-growing lending app: 50,000 applications/month with 3-5% fraud rate via manual KYC. After eKYC: fraud below 0.5%, loan approval time drops from 2 days to 4 hours. A direct competitive advantage in Vietnam's active fintech sandbox environment.

Scenario 3 - Digital insurance: Video call onboarding takes 45 minutes per customer, with 40% abandon rate. After eKYC: 3 minutes per customer, abandon rate drops to 15%. With 5,000 leads/month, that's 1,250 additional customers completing onboarding every month.

6 Criteria for Choosing the Right eKYC API for Vietnam

- Accuracy on Vietnamese ID documents: OCR and face matching must be trained on Vietnamese data - chip-embedded CCCD, old 9-digit IDs, passports. Request a demo with sample documents from multiple provinces.

- VNeID / C06 database integration: Cross-verification with the national citizen database is a required SBV standard.

- Latency & SLA: Under 3 seconds for full verification flow; 99.9% uptime SLA.

- PDPL & AI Law compliance documentation: Vendor must provide a Data Processing Agreement (DPA) that meets PDPL standards - not just verbal assurances.

- Pricing model for your volume: Calculate TCO at some levels: 5,000 / 20,000 / 100,000 verifications per month.

- Free sandbox environment: A free integration sandbox before signing is a sign the vendor is confident in their product.

DataCore eKYC: API Built for the Vietnamese Market

DataCore eKYC API is built on DataCore's 8-year data infrastructure - combining a CCCD OCR engine, face matching with liveness detection, and cross-checking with Vietnam's company and credit databases.

- PDPL-native: Zero-retention architecture by default - no raw biometric data stored after verification

- Vietnam-first model: OCR and face matching optimized for chip-embedded CCCD and Vietnamese passports

- Free sandbox: Test integration before signing any contract

What to Expect When Moving to eKYC Vietnam

Teams adopting eKYC Vietnam usually phase the rollout: start with a single product line, run eKYC Vietnam alongside the existing manual check for a short period, then switch fully once match rates and fraud-capture are proven. This staged approach protects conversion while the team builds confidence in the automated decision.

The operational win is not only speed. A properly instrumented eKYC Vietnam flow produces a structured, timestamped record of every verification, which turns compliance reporting from a manual scramble into a query. That audit trail is increasingly what regulators and banking partners expect to see before they will work with a fintech.

The takeaway for 2026 is straightforward: manual onboarding still works for tiny volumes, but for any team planning to scale, eKYC Vietnam is the option that keeps cost, speed, and compliance moving in the same direction instead of trading one against another.

For more 2026 analysis on identity, onboarding, and compliance in Vietnam, see the DataCore news and insights hub, updated regularly for product and risk teams.

Frequently Asked Questions About eKYC Vietnam

Is eKYC Vietnam legally compliant in 2026?

Yes. Under Decree 94/2025/ND-CP, the Personal Data Protection Law, and the AI Law, eKYC Vietnam is recognised for remote onboarding provided the provider meets data-protection and automated-verification standards and retains an auditable record of each check.

How much faster is eKYC Vietnam than manual onboarding?

Manual onboarding typically takes days; a well-built eKYC Vietnam flow completes identity verification in under a minute, which is the single largest driver of reduced application drop-off.

Does eKYC Vietnam reduce fraud?

It can, when liveness detection and face match are combined. eKYC Vietnam systems catch deepfake and document-forgery attempts that manual reviewers routinely miss, while logging every decision for audit.

Conclusion: The Decision Point Is Now

The question is no longer "should we switch to eKYC?" - it's "do we switch now, or wait until we're forced to in a harder situation?" Three pressures are converging: regulatory risk from PDPL and AI Law; competitive pressure in Vietnam's growing fintech sandbox ecosystem; and economic pressure to reduce costs while improving quality simultaneously.

Get started with DataCore eKYC API - free sandbox to test integration: datacore.vn/en/services/ekyc or contact hello@datacore.vn for a consultation and volume-based pricing.

Để lại một bình luận

You must be logged in to post a comment.